Global Pharmaceutical Contract Sales Outsourcing (CSO) Market Analysis

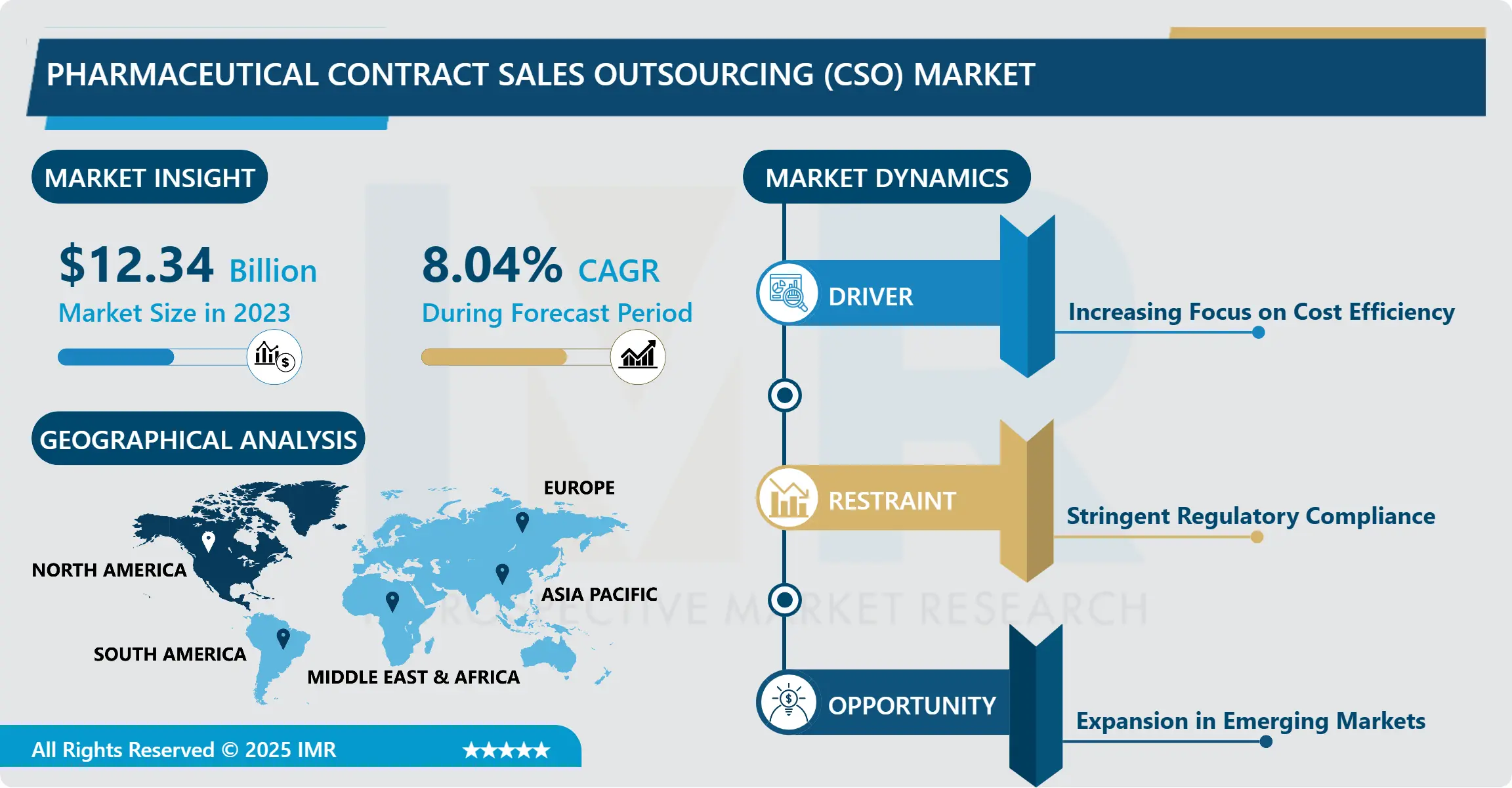

The Global Pharmaceutical Contract Sales Outsourcing (CSO) Market Size Was Valued at USD 12.34 Billion in 2023 and is Projected to Reach USD 24.75 Billion by 2032, Growing at a CAGR of 8.04% From 2024-2032.

Pharmaceutical Contract Sales Outsourcing (CSO) refers to the strategic practice where pharmaceutical and biotechnology companies hire third-party organizations to manage their sales and marketing activities. These services range from providing specialized sales forces and medical representatives to handling market access, clinical detailing, and digital promotion. By leveraging a CSO, pharmaceutical firms can rapidly deploy experienced sales teams without the long-term overhead of permanent staff, allowing them to focus resources on core research and development (R&D) and manufacturing activities.

The primary advantage of CSO services over traditional in-house sales forces is the high degree of operational flexibility and cost-efficiency they offer. Pharmaceutical companies can scale their sales efforts up or down based on product launch cycles, patent expirations, or regional market shifts. Furthermore, CSOs often possess deep local market expertise and established physician networks, which are crucial for navigating complex regulatory landscapes. Major industries utilizing CSO services include large-cap pharmaceutical corporations, mid-sized biotech firms, and emerging healthcare startups. The increasing complexity of drug portfolios and the rising costs of internal sales management are significant drivers for the market's continued expansion.

👉 To request a sample report:

https://introspectivemarketresearch.com/request/20249

Market Segmentation

The Pharmaceutical Contract Sales Outsourcing (CSO) Market is segmented into Service Type, Therapeutic Area, and End-User. By Service Type, the market is categorized into (Personal Selling, Non-Personal Selling, Market Access, Other Services). By Therapeutic Area, the market is categorized into (Oncology, Cardiovascular, Neurology, Metabolic Disorders, Others). By End-User, the market is categorized into (Pharmaceutical Companies, Biotechnology Companies, Medical Device Companies).

Growth Driver

The principal growth driver for the Pharmaceutical CSO Market is the escalating cost of drug development combined with the need for specialized sales expertise for complex therapies. As the industry shifts toward "specialty" drugs such as biologics and personalized medicines for rare diseases—sales teams require higher levels of clinical knowledge and technical detailing. Maintaining such specialized teams in-house is prohibitively expensive for many firms. CSOs provide a solution by offering "on-demand" expertise, allowing companies to mitigate financial risks during product launches while ensuring that high-value therapies reach the right medical professionals and patient populations efficiently.

Market Opportunity

A major market opportunity lies in the rapid digital transformation of sales outreach and the rise of "omnichannel" marketing strategies. The post-pandemic landscape has permanently altered how medical representatives interact with healthcare providers (HCPs), with a significant increase in virtual detailing and digital engagement. CSOs that integrate advanced data analytics and AI-driven CRM tools to optimize these digital touchpoints represent a high-growth frontier. By providing data-backed insights into HCP behavior and preferences, CSOs can offer pharmaceutical clients a more personalized and effective sales strategy, bridging the gap between physical and digital promotion in an increasingly crowded therapeutic market.

Detailed Segmentation

Title: Pharmaceutical Contract Sales Outsourcing (CSO) Market Market, Segmentation The Pharmaceutical Contract Sales Outsourcing (CSO) Market is segmented on the basis of Service Type, Therapeutic Area, and End-User.

Service Type

The Service Type segment is further classified into Personal Selling, Non-Personal Selling, and Market Access. Among these, the Personal Selling sub-segment accounted for the highest market share in 2023. Personal selling, which involves face-to-face interactions between medical representatives and healthcare providers, remains the cornerstone of pharmaceutical marketing. Despite the rise of digital tools, the "human touch" and the ability to build trust through clinical discussion are irreplaceable for high-stakes therapeutic decisions. The reliability of personal selling for establishing long-term relationships with key opinion leaders (KOLs) and specialist physicians ensures its continued dominance as the primary revenue generator for CSOs.

End-User

The End-User segment is further classified into Pharmaceutical Companies, Biotechnology Companies, and Medical Device Companies. Among these, the Pharmaceutical Companies sub-segment accounted for the highest market share in 2023. Large and mid-cap pharmaceutical firms are the largest consumers of CSO services due to their extensive and diverse product pipelines. These organizations frequently utilize outsourcing to manage "legacy" brands or to support secondary indications, allowing their internal teams to focus exclusively on flagship blockbusters. The continuous need to maintain market share across multiple regions and therapeutic categories drives these companies to partner with CSOs for scalable and specialized sales support.

Some of The Leading or Active Market key Players Are-

· IQVIA Inc. (United States)

· Syneos Health (United States)

· Ashfield (UDG Healthcare) (Ireland)

· Publicis Health (France)

· Inizio (United Kingdom)

· EVERSANA (United States)

· Indegene (India)

· APL (Zuelig Pharma) (Singapore)

· Pharmexx (Germany)

· Amplity Health (United States)

· and other active players.

Key Industry Developments

In June 2024, (Bold) IQVIA Inc. announced the enhancement of its "Orchestrated Commercial Lead" platform, integrating generative AI to provide real-time sales recommendations for outsourced medical representatives. This development is significant as it allows CSO teams to utilize predictive analytics to identify the most receptive healthcare providers, thereby increasing the efficiency and conversion rates of sales calls in competitive therapeutic markets.

In February 2024, (Bold) Syneos Health completed a strategic partnership with a major European biotech firm to manage the full-scale commercial launch of a new orphan drug. This development is significant because it highlights the growing trend of "Full-Service" outsourcing, where CSOs handle everything from market access and payer negotiations to regional sales force deployment, showcasing the evolving role of CSOs as end-to-end commercial partners.

Key Findings of the Study

· Dominant Segments: Personal Selling (Service Type) and Pharmaceutical Companies (End-User) remain the primary drivers of market revenue.

· Leading Regions: North America leads the market due to its high concentration of pharmaceutical giants and a mature outsourcing ecosystem.

· Key Growth Drivers: Rising costs of internal sales forces and the increasing complexity of specialty drug portfolios.

· Market Trends: A significant shift toward hybrid sales models combining traditional personal selling with AI-powered digital detailing tools.

🔍 𝐈𝐧-𝐃𝐞𝐩𝐭𝐡 𝐑𝐞𝐩𝐨𝐫𝐭:

About Introspective Market Research

Introspective Market Research is a global provider of data-driven market intelligence and strategic advisory services. Our analysts and consultants deliver comprehensive reports, actionable insights and customized consulting to clients across chemicals & materials, healthcare, energy, environment, infrastructure, and advanced manufacturing sectors.

Media Contact:

Introspective Market Research.

Email: press@introspectivemarketresearch.com

Website: http://www.introspectivemarketresearch.com

Phone: +91-91753-37569