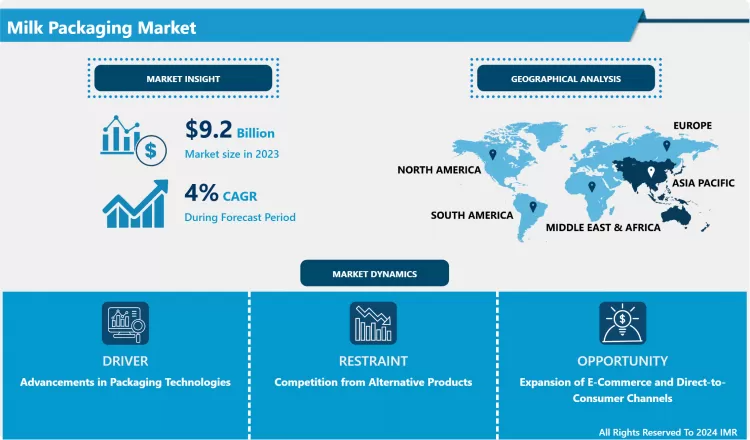

The Global Milk Packaging Market Size Was Valued at USD 9.2 Billion in 2023 and is Projected to Reach USD 13.21 Billion by 2032

The Global Milk Packaging Market Size Was Valued at USD 9.2 Billion in 2023 and is Projected to Reach USD 13.21 Billion by 2032, Growing at a CAGR of 4%.

Milk packaging involves specialized container solutions primarily cartons, bottles, and pouches designed to protect milk from contamination, light exposure, and bacterial growth, thereby preserving its nutritional value and extending its shelf life. The market is driven by packaging that must meet stringent food safety standards while optimizing storage and transport logistics for a highly perishable product. This packaging ensures safety and quality from the dairy farm to the consumer's table, often incorporating specialized barrier layers (such as aluminium or polymers) to maintain freshness.

The primary advantage of modern milk packaging, especially multi-layer paperboard cartons and aseptic plastic bottles, over traditional glass bottles is significantly extended shelf stability without refrigeration (UHT milk) and reduced breakage risk. Aseptic processing and packaging allow milk to be stored safely for months, opening up global distribution channels and minimizing food waste. Main uses include high-volume retail for fresh and extended shelf-life (ESL) milk, dairy alternatives (e.g., oat, almond milk), and institutional supply chains (schools, hospitals) that require secure, portion-controlled containers.

👉 To request a sample report

https://introspectivemarketresearch.com/request/18274

Market Segmentation

The Milk Packaging Market is segmented into Material, Type, and End-user. By Material, the market is categorized into (Plastic, Paperboard, Glass, Metal). By Type, the market is categorized into (Bottles, Pouches, Cartons, Cups). By End-user, the market is categorized into (Retail, Institutional, Industrial).

Growth Driver

The principal driver for market expansion is the continuous, escalating global demand for Extended Shelf-Life (ESL) and Ultra-High Temperature (UHT) treated milk products. These treatments require highly protective, aseptic packaging solutions, predominantly multi-layer cartons and specialized barrier plastic bottles, to maintain sterility and prevent spoilage over several months without refrigeration. This allows dairy companies to access vast, previously untapped markets, especially in regions with poor cold chain infrastructure. The investment in advanced barrier packaging technology directly facilitates this geographic expansion and shelf stability, cementing its role as a core growth mechanism.

Market Opportunity

A major market opportunity is the rapid innovation and adoption of sustainable packaging materials and formats in response to increasing consumer and regulatory pressure against single-use plastics. This includes the shift towards bio-based barrier polymers, plant-derived carton coatings, and fully recyclable paperboard structures. Companies are actively investing in new cap designs and lightweight materials that reduce carbon footprint while maintaining product integrity. This focus on eco-friendly alternatives provides a significant competitive edge and a high-growth pathway for manufacturers who can commercialize effective, high-barrier, sustainable milk packaging solutions.

Detailed Segmentation

Title: Milk Packaging Market, Segmentation Line below: The Milk Packaging Market is segmented on the basis of Material, Type, and End-user.

By Material

The Material segment is further classified into Plastic, Paperboard, Glass, and Metal. Among these, the Paperboard sub-segment accounted for the highest market share in 2023. Paperboard dominates due to its widespread adoption in aseptic and ESL packaging formats, offering excellent light and oxygen barrier protection when laminated with foil or polymers. Its lightweight nature, efficient cube utilization, and consumer perception as a renewable and recyclable material make it the material of choice for high-volume milk and dairy-alternative packaging globally. Furthermore, the printable surface provides ample space for branding and regulatory information.

By Type

The Type segment is further classified into Bottles, Pouches, Cartons, and Cups. Among these, the Cartons sub-segment accounted for the highest market share in 2023. Cartons, including gable top and brick-style aseptic formats, command the largest share driven by their structural rigidity, stacking efficiency, and crucial role in facilitating UHT/ESL distribution. Their rectangular shape minimizes wasted space during transport and storage, while the multi-layer barrier structure is essential for preserving the milk's quality for months. This combination of logistical efficiency and superior product protection makes cartons the preferred format for both fresh and shelf-stable milk in retail environments worldwide.

Some of The Leading or Active Market key Players Are-

Tetra Pak (Switzerland) Elopak Group (Norway) Amcor plc (Switzerland/Australia) Berry Global Group, Inc. (United States) Mondi plc (United Kingdom/South Africa) DS Smith Plc (United Kingdom) SIG Combibloc Group AG (Switzerland) Sealed Air Corporation (United States) Huhtamaki Oyj (Finland) Greatview Aseptic Packaging Co., Ltd. (China) Evergreen Packaging (United States) Smurfit Kappa Group (Ireland) WestRock Company (United States) Winpak Ltd. (Canada) Ball Corporation (United States) and other active players.

Key Industry Developments

In March 2024, Tetra Pak invested heavily in R&D to commercialize a fiber-based barrier for milk cartons, replacing the conventional aluminum foil layer. This project is aimed at achieving a significant milestone in packaging sustainability by making the carton structure more easily renewable and recyclable. The new fiber barrier technology maintains the necessary shelf-life protection against light and oxygen, positioning the company at the forefront of the circular economy trend and responding to mounting pressure for better end-of-life solutions for multi-layer packaging.

In January 2024, a consortium of European dairy producers and packaging firms launched a pilot program to standardize recycling infrastructure for difficult-to-recycle milk pouches. This initiative focuses on the collection and reprocessing of thin-film plastic pouches, which are widely used for affordable, fresh milk delivery in several regions but often lack proper disposal pathways. The pilot aims to close the loop on this popular format, demonstrating a viable economic model for recycling and expanding the adoption of milk pouches as a low-cost, low-material-use option.

Key Findings of the Study

· Dominant Segments: Paperboard material and the Cartons type lead the market, fueled by aseptic packaging technology.

· Leading Regions: The Asia Pacific region is expected to show the fastest growth due to expanding consumption of shelf-stable UHT milk.

· Key Growth Drivers: Mandates for extended product shelf-life and enhanced global food safety standards are the core drivers.

· Market Trends: Rapid innovation in fully recyclable, bio-based barrier materials is currently the most impactful trend.

🔍 𝐈𝐧-𝐃𝐞𝐩𝐭𝐡 𝐑𝐞𝐩𝐨𝐫𝐭:

https://introspectivemarketresearch.com/reports/milk-packaging-market/

About Introspective Market Research

Introspective Market Research is a global provider of data-driven market intelligence and strategic advisory services. Our analysts and consultants deliver comprehensive reports, actionable insights and customized consulting to clients across chemicals & materials, healthcare, energy, environment, infrastructure, and advanced manufacturing sectors.

Media Contact:

Introspective Market Research.

Email: press@introspectivemarketresearch.com

Website: http://www.introspectivemarketresearch.com

Phone: +91-91753-37569